Futures Market: Overnight, LME copper opened at $8,891/mt, dipped to $8,872/mt at the beginning of the session, surged to $9,076/mt during the session, and slightly pulled back to close at $8,966/mt, up 0.82%. Trading volume reached 28,000 lots, and open interest stood at 282,000 lots. Overnight, the most-traded SHFE copper 2502 contract opened at 74,530 yuan/mt, peaked at 74,680 yuan/mt early in the session, dropped to 74,250 yuan/mt during the session, and rebounded before consolidating sideways to close at 74,500 yuan/mt, up 1.14%. Trading volume reached 50,900 lots, and open interest stood at 148,000 lots.

【SMM Copper Morning Briefing】News: (1) According to The Washington Post, three individuals familiar with the matter revealed that aides to US President-elect Trump are exploring a tariff plan applicable to "all countries" but limited to key imported goods, marking a significant shift in Trump's 2024 presidential campaign strategy.

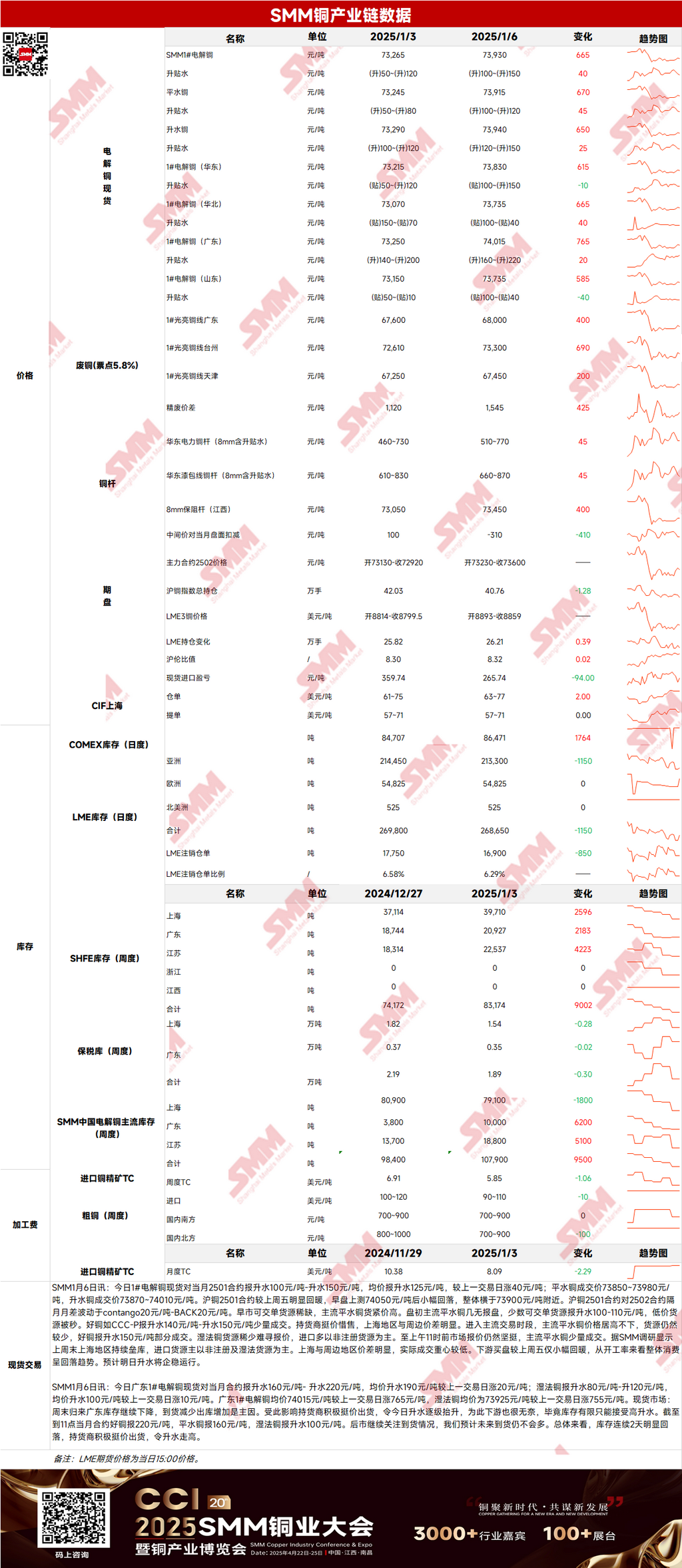

Spot Market: (1) Shanghai: On January 6, mainstream standard-quality copper premiums against the front-month contract were quoted at 100-120 yuan/mt, while high-quality copper premiums were at 120-150 yuan/mt. According to the SMM survey, inventory buildup continued in Shanghai over the weekend, with imported supplies mainly consisting of non-registered and hydro copper. There was a significant price spread between Shanghai and surrounding regions, and actual transaction centers were relatively low. Downstream buying slightly improved compared to last Friday, but overall consumption showed a downward trend based on operating rates. Premiums are expected to stabilize tomorrow.

(2) Guangdong: On January 6, #1 copper cathode spot premiums against the front-month contract were quoted at 160-220 yuan/mt, with an average premium of 190 yuan/mt, up 20 yuan/mt from the previous trading day. Hydro copper premiums were at 80-120 yuan/mt, with an average premium of 100 yuan/mt, up 10 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 74,015 yuan/mt, up 765 yuan/mt from the previous trading day, while hydro copper averaged 73,925 yuan/mt, up 755 yuan/mt. Overall, inventory has significantly declined for two consecutive days, and suppliers actively stood firm on quotes, pushing premiums higher.

(3) Imported Copper: On January 6, warehouse warrant prices ranged from $63 to $77/mt, QP January, with an average price up $2/mt from the previous trading day. B/L prices ranged from $57 to $71/mt, QP February, with the average price unchanged from the previous trading day. EQ copper (CIF B/L) was quoted at $12-26/mt, QP February, with the average price also unchanged from the previous trading day. Quotes referenced cargoes arriving in mid-to-late January and early February. During the day, warehouse warrant and B/L quotes were scattered, with limited transactions for Date-front B/L. Prices for bonded warehouse warrants remained high, but actual transactions were also inactive. Overall, the SHFE/LME price ratio weakened, and market activity was low.

(4) Secondary Copper: On January 6, secondary copper raw material prices rose by 400 yuan/mt MoM. Guangdong bare bright copper prices were 67,900-68,100 yuan/mt, up 400 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,545 yuan/mt, up 425 yuan/mt MoM. The price spread for rods was 495 yuan/mt. According to the SMM survey, although copper prices rebounded and the price difference between primary metal and scrap widened, secondary copper raw material suppliers held low inventories, and shipments did not significantly increase. Transactions for secondary copper raw materials remained flat in recent days.

(5) Inventory: On January 6, LME copper cathode inventory decreased by 1,150 mt to 268,650 mt. SHFE warehouse warrant inventory decreased by 2,442 mt to 15,652 mt.

Prices: On the macro side, copper prices rose sharply as US media reported that Trump would implement universal tariffs only on key imported goods, causing the US dollar index to plunge. However, Trump later posted on social media denying the accuracy of the tariff policy reports, leading to a rebound in the US dollar index and capping copper price gains. On the fundamentals side, the supply of copper cathode in the market remained tight, with imported supplies mainly consisting of non-registered and hydro copper. As of Monday, January 6, SMM data showed that copper inventories in major regions across China increased by 1,500 mt from last Thursday to 115,800 mt, up 42,900 mt compared to the same period last year (72,900 mt). This week, as it is the beginning of the year, downstream enterprises are expected to have sufficient funds, leading to a potential increase in operating rates and a likely decline in weekly inventories. In terms of prices, US Fed Governor Cook stated that interest rate cuts could be approached more cautiously. With multiple Fed officials speaking and economic data releases scheduled this week, the US dollar index is expected to remain strong, posing resistance to copper prices.

》Click to view the SMM Metal Database.

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】